Momentum Calculations#

Momentum Calculations#

This article will explore various methods for assessing momentum in financial markets.

[2]:

from statsmodels import regression

import statsmodels.api as sm

import scipy.stats as stats

import scipy.spatial.distance as distance

import matplotlib.pyplot as plt

import pandas as pd

import numpy as np

# import auquanToolbox.dataloader as dl

Using Moving Averages to Spot Momentum#

A common way to figure out if something is gaining or losing momentum is by looking at moving averages. This involves calculating two different types of averages and seeing when they cross paths. Depending on which one crosses the other, we can tell if momentum is going up or down.

Let’s take a look at how this works with real data from assets.

[73]:

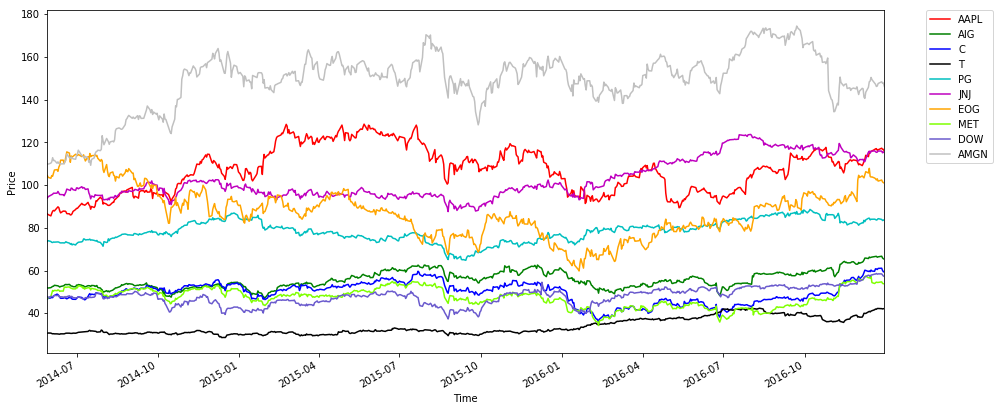

# Fetch prices data for 10 stocks from different sectors and plot prices

start = '2014-06-01'

end = '2016-12-31'

assets = ['AAPL', 'AIG', 'C', 'T', 'PG', 'JNJ', 'EOG', 'MET', 'DOW', 'AMGN']

data = dl.load_data_nologs('nasdaq', assets, start, end)

prices = data['ADJ CLOSE']

prices.plot(figsize=(15,7), color=['r', 'g', 'b', 'k', 'c', 'm', 'orange',

'chartreuse', 'slateblue', 'silver'])

plt.legend(bbox_to_anchor=(1.05, 1), loc=2, borderaxespad=0.)

plt.ylabel('Price')

plt.xlabel('Time')

plt.show()

Reading AAPL

Reading AIG

Reading C

Reading T

Reading PG

Reading JNJ

Reading EOG

Reading MET

Reading DOW

Reading AMGN

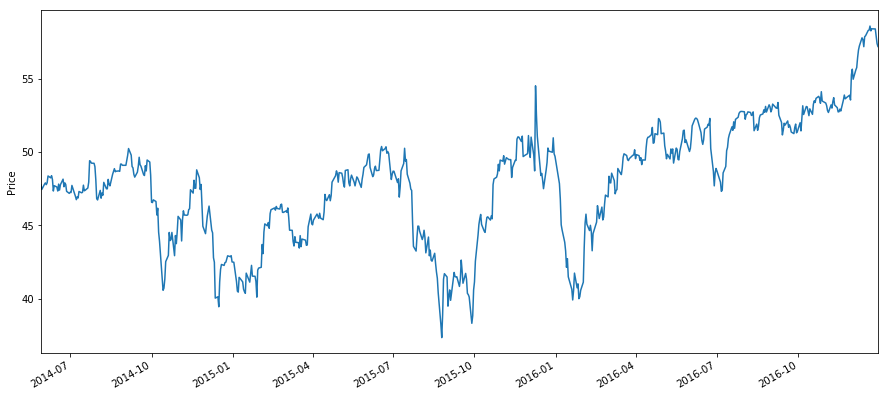

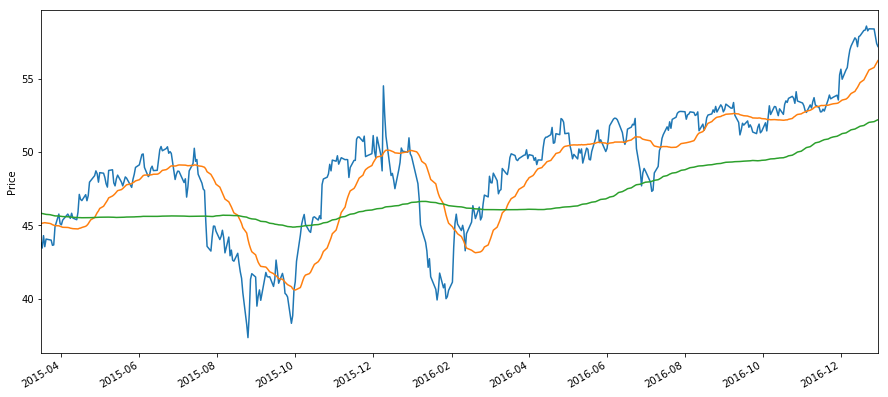

Nowlet’s pick a stock and calculate a 30 day moving average and a 200 day moving average.

[74]:

asset = prices.iloc[:, 8]

asset.plot(figsize=(15,7))

plt.ylabel('Price')

plt.show()

[75]:

short_mavg = asset.rolling(window=30, center=False).mean()

long_mavg = asset.rolling(window=200, center=False).mean()

asset[200:].plot(figsize=(15,7))

short_mavg[200:].plot()

long_mavg[200:].plot()

plt.ylabel('Price')

plt.show()

We can see here that there are five crossing points once both averages are fully populated. The first seems to be indicative of a following upturn, second of a downturn and so on.

Choosing Moving Average Lengths#

WARNING: Overfitting#

The choice of lengths will strongly affect the signal that you receive from your moving average crossover strategy. There may be better windows, and attempts to find them can be made with robust optimization techniques. However, it is incredibly easy to overfit your moving window lengths. For an exmaple of this see the Dangers of Overfitting.

Moving Average Crossover Ribbons#

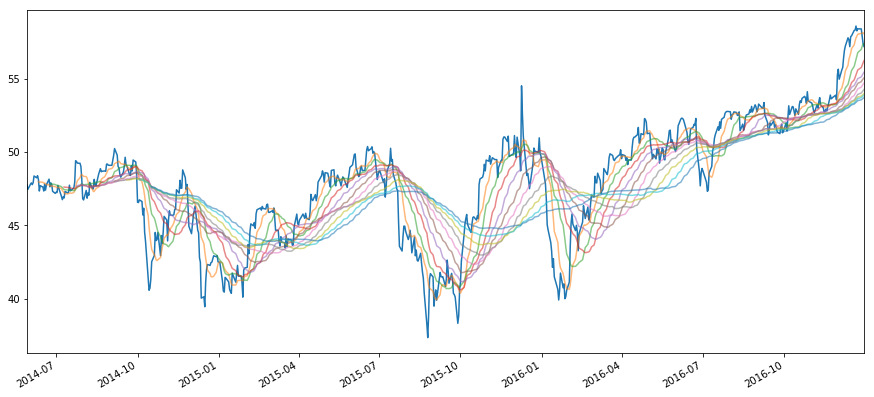

Another approach is to draw many moving averages at a time, and attempt to extract statistics from the shape of the ‘ribbon’ rather than any two moving averages. Let’s see an example of this on the same asset.

[77]:

asset.plot(alpha = 1)

rolling_means = {}

for i in np.linspace(10, 100, 10):

X = asset.rolling(window=int(i),center=False).mean()

rolling_means[i] = X

X.plot(figsize=(15,7), alpha = 0.55)

rolling_means = pd.DataFrame(rolling_means).dropna()

plt.show()

Information About Ribbon Shape#

Here are a few quantitative measures of ribbon shape. This will in turn give us a trading signal.

Distance Metric#

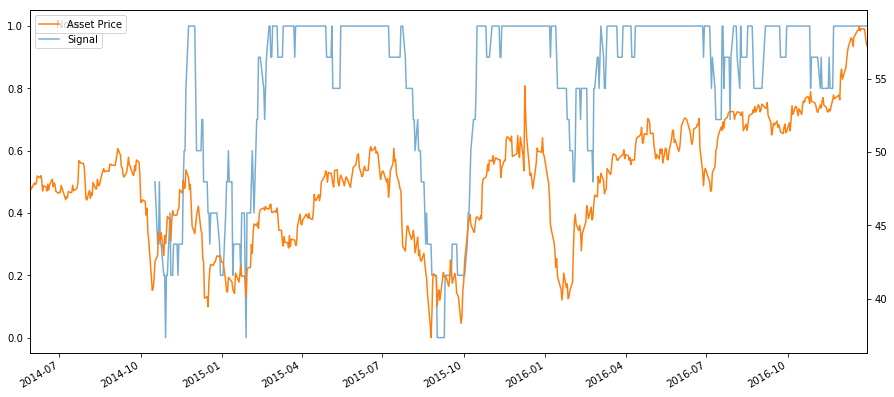

We can use a distance metric to see how far away from some given ranking our ribbon is. Here we check against a 1-10 ranking. * A perfectly increasing order of ribbons (i.e 10d MA < 20d MA <… 100d MA) results in a score of 0. This can be a signal to buy to go long. * A perfectly decreasing order of ribbons (i.e 10d MA > 20d MA >… 100d MA) results in a score of 1. This can be a signal to sell to go short.

For more ideas on distance metrics, check out this slide deck.

[104]:

scores = pd.Series(index=asset.index)

for date in rolling_means.index:

mavg_values = rolling_means.loc[date]

ranking = stats.rankdata(mavg_values.values)

d = distance.hamming(ranking, range(1, 11))

scores[date] = d

# Normalize the score

(scores).plot(figsize=(15,7), alpha=0.6)

plt.legend(['Signal'], bbox_to_anchor=(1.25, 1))

asset.plot(secondary_y=True, alpha=1)

plt.legend(['Asset Price'])

plt.show()

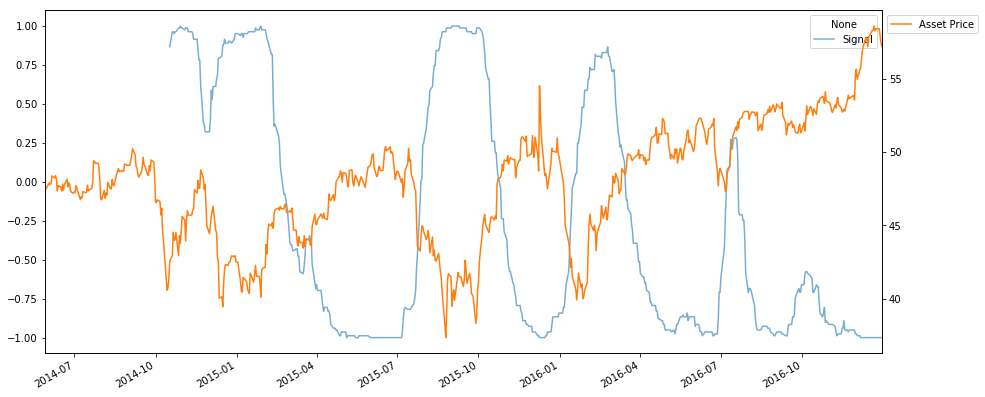

We can also use a correlation metric * A perfectly increasing order of ribbons (i.e 10d MA < 20d MA <… 100d MA) results in a score of 1. This can be a signal to buy to go long. * A perfectly decreasing order of ribbons (i.e 10d MA > 20d MA >… 100d MA) results in a score of -1. This can be a signal to sell to go short.

[109]:

scores = pd.Series(index=asset.index)

for date in rolling_means.index:

mavg_values = rolling_means.loc[date]

ranking = stats.rankdata(mavg_values.values)

d, _ = stats.spearmanr(ranking, range(1, 11))

scores[date] = d

# Normalize the score

(scores).plot(figsize=(15,7), alpha=0.6);

plt.legend(['Signal'], bbox_to_anchor=(1, 0.9))

asset.plot(secondary_y=True, alpha=1)

plt.legend(['Asset Price'], bbox_to_anchor=(1, 1))

plt.show()

Measuring Thickness#

We can also just take the range of values at any given time to monitor the thickness of the ribbon. Thick riboons indicate a buy or sell trading signal (the moving averages diverge from one another). Combine this with difference in Moving Averages to buy or sell.

[110]:

scores = pd.Series(index=asset.index)

for date in rolling_means.index:

mavg_values = rolling_means.loc[date]

d = np.max(mavg_values) - np.min(mavg_values)

scores[date] = d

# Normalize the score

(scores).plot(figsize=(15,7), alpha=0.6);

plt.legend(['Signal'], bbox_to_anchor=(1, 0.9))

asset.plot(secondary_y=True, alpha=1)

plt.legend(['Asset Price'], bbox_to_anchor=(1, 1))

plt.show()

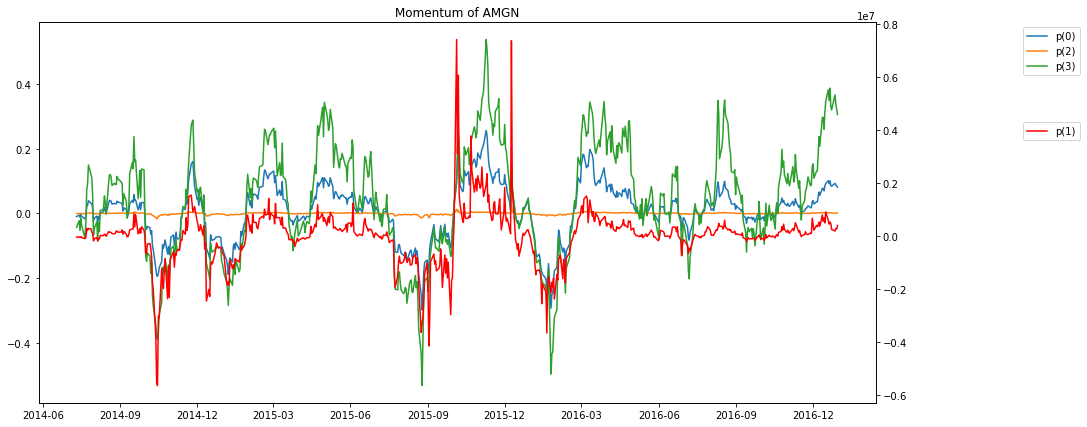

Measures of Momentum From Physics#

Here we present some measures of momentum taken from physics. The paper describing these measures can be found here http://arxiv.org/pdf/1208.2775.pdf. The authors define 4 different measures, called \(p^{(1)}\), \(p^{(0)}\), \(p^{(2)}\), and \(p^{(3)}\).

Their approach is based in physics, where the momentum is defined as \(p = mv\), the product of the mass and the velocity. First, they define \(x(t)\) to be the log of the price of the security. Conveniently, the return on the security is then the derivative of \(x(t)\), which is called the velocity \(v(t)\). Then they suggest a number of different definitions of mass \(m(t)\); in the examples below, we’ll use the inverse of standard deviation and turnover rate as mass. This works with our analogy because the more volatile or the less liquid an asset (the smaller its mass), the easier it is to move its price (i.e. change its position). The different momenta are then defined (for a lookback window \(k\)) as:

First, let’s just implement the different momentum definitions, and plot the rolling momenta for one stock.

[46]:

k = 30

start = '2014-01-01'

end = '2015-01-01'

x = np.log(asset)

v = x.diff()

m = data['VOLUME'].iloc[:,8]

p0 = v.rolling(window=k, center=False).sum()

p1 = m*v.rolling(window=k, center=False).sum()

p2 = p1/m.rolling(window=k, center=False).sum()

p3 = v.rolling(window=k, center=False).mean()/v.rolling(window=k, center=False).std()

[111]:

f, ax1 = plt.subplots(figsize=(15,7))

ax1.plot(p0)

ax2 = ax1.twinx()

ax2.plot(p1,'r')

ax1.plot(p2)

ax1.plot(p3)

ax1.set_title('Momentum of AMGN')

ax1.legend(['p(0)', 'p(2)', 'p(3)'], bbox_to_anchor=(1.25, 1))

ax2.legend(['p(1)'], bbox_to_anchor=(1.25, .75))

plt.show()

Going forward#

What are good lookback and holding period lengths? We picked 30 days as a reasonable default but others might make more sense (or even different lengths for the different momentum definitions). Be careful not to overfit here!

Try different definitions of mass. The paper suggests turnover rate and daily transaction value (and volatility is only used for \(p^{(3)}\)).